Current trends in electronic payments

Contactless payments

Today, most stores in Austria already offer the option to pay contactless using a debit or credit card, a smartphone, or a smartwatch. This is made possible by the NFC (Near Field Communication) transmission standard and does not require entering a PIN. To make a payment, the card or mobile device simply needs to be held very close to the payment terminal. Terminals that support contactless payments, as well as cards that allow for such payments, can typically be identified by a small wireless symbol displayed on the terminal or card.

Background information: Near Field Communication, or NFC, is a transmission standard for contactless communication between electronic devices over short distances (max. 4 cm).

Sharp increase in contactless payments since 2020

Contactless payment is now widespread not only in the USA and Asia but also in Europe. In Austria, contactless payments accounted for 95% of all debit card transactions at the point of sale by the end of 2024.

Contactless card payments

Instead of inserting the card into the terminal, it is held close to the terminal to initiate the payment. For contactless card payments, entering a PIN is only required for amounts over 50 EUR or after multiple payments totaling 125 EUR have been made. Even for amounts above 50 EUR, the card does not need to be inserted into the terminal, but PIN entry is still mandatory. Whether the card is used contactlessly or not, the payment processing in the background remains unchanged.

Contactless mobile payments

Some banks offer their customers the option to digitize their payment card onto a smartphone or smartwatch, enabling contactless payments using these devices. The card is stored in a virtual wallet (e.g., Google Pay or Apple Pay), and multiple cards can be added to the same wallet.

There are also mobile payment solutions that do not rely on a payment card. These solutions often use QR codes instead of NFC. The QR code can be scanned either by the merchant or the customer. Such solutions (e.g., Bluecode) have been available in Austria for several years.

Paying in online retail

Online retail has been growing steadily for quite some time, and this trend accelerated during the COVID-19 lockdown phases due to limited in-person shopping opportunities. According to the Austrian Retail Association, online retail spending in Austria reached a new record of EUR 10.6 billion in 2024 — a 5% increase over the previous year.

One key factor behind this boom is the growing acceptance of digital payment methods among both retailers and consumers. In addition to traditional bank transfers and credit card payments, users can now choose from an increasingly diverse and user-friendly range of wallets and online payment methods.

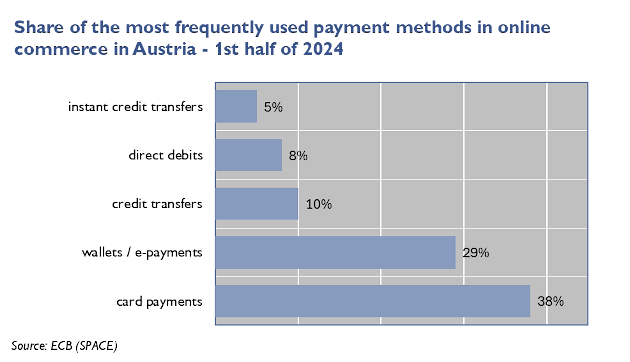

In Austria, the most frequently used payment methods in online shopping are card payments (38%), wallets and internet-based payment systems (29%), and bank transfers (10%). Direct debits (8%) and instant payments (5%) play a lesser role in online retail.

What are instant payments?

The SEPA Instant Credit Transfer is a new payment instrument that European banks have been able to offer to their customers since November 2017 – and will be required to offer starting in October 2025. Unlike standard transfers, which typically take around one business day to process, instant payments are available in just a few seconds in the recipient’s account – 24/7, including weekends and public holidays.

More information on SEPA Instant Payments can be found here