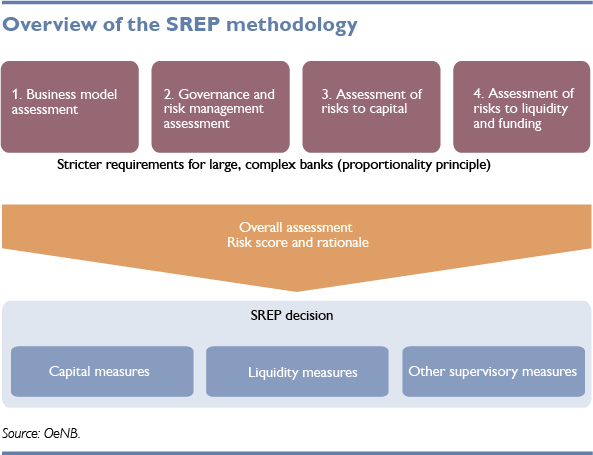

SREP – Supervisory Review and Evaluation Process

One of the key tasks of banking supervision is to ensure the overall viability and sustainability of credit institutions. In particular, each bank needs:

- an effective business model

- adequate risk management systems

- a solid capital base

- adequate liquidity and funding position

These four main factors are assessed as part of the annual Supervisory Review and Evaluation Process (SREP), taking into account a multi-year assessment (MYA). This means that a holistic approach is used to assess banks’ risks, but with varying degrees of intensity and, as appropriate, at lower frequencies, in accordance with the risk tolerance framework (RTF).

What issues does the SREP address?

1. The business model analysis covers the bank’s core business, its economic environment and its funding plan. The focus is on adequate profitability as well as on the sustainability of the business model, with a view to ensuring that banks are able to meet potential or existing capital shortfalls without external aid. If the SREP review shows that the business model is deficient or that restructuring plans may aggravate a bank’s financial situation, possible measures will be discussed with the bank and imposed as necessary.

2. The assessment of governance seeks to establish whether the risk management function is adequately staffed and qualified, and whether it operates independently from the decision-making units about lending, i.e. those that take on risk. Additionally, the SREP verifies whether internal audits have been conducted as required, whether remuneration policies and practices comply with legal requirements and whether internal processes are adequately designed for the complexity of the bank’s operations. Mechanisms must be in place to ensure that management is informed in a timely manner and involved in the decision-making process.

3. The third part involves evaluating risks that could lead to losses and therefore adequate capital needs to be ensured. Specifically, the SREP verifies whether all risks have been identified, measured and covered with adequate capital.

Austrian banks primarily face credit risk from traditional lending activities, essentially the risk from unexpected defaults by private and corporate customers. Additionally, there are other risks such as changes in interest rate and market prices, currency fluctuations, IT risks or legal risks. In general, riskier transactions will entail higher capital requirements than less risky transactions. At the same time, weak control of existing risks and/or inadequate risk management processes may also lead to a worse assessment and subsequently higher capital requirements.

Within the SREP framework, supervisors check banks’ self-assessment against regulatory requirements and assess whether banks’ own risk assessments are complete and adequately conservative. Supervisors perform plausibility checks of budget numbers and possible future challenges and challenge banks’ calculations against supervisory calculations. Moreover, supervisors take into account any other relevant information on potential deficiencies gathered through on-site analysis or other sources.

In this way, they review all types of risk in detail and report identified weaknesses back to banks. The SREP process also checks the plausibility of reported data to identify data quality problems. In addition, it takes into account supervisory stress tests results identifying bank-specific vulnerabilities.

If necessary, banks may be required to take appropriate measures and ensure that they hold adequate capital.

4. Supervisors also analyze risks to banks’ liquidity and funding, which may render them unable to meet their payment obligations in a timely manner. These assessments address both short-term excess liquidity and long-term funding plans. In addition, supervisors assess the outcome of their stress tests to ensure that banks have enough liquidity even under more adverse external conditions. One way to ensure this is to require banks to invest excess liquidity over short-term horizons, enabling them to respond swiftly to changes in the business environment.

What are the possible outcomes of the overall SREP assessment?

Taking into account the size and complexity of the institutions concerned as well as the MYA (multi-year assessments), analysts aggregate the individual results at the end of the process, producing an overall SREP assessment. This serves as a basis for the decision by the Financial Market Authority (FMA) or the ECB to set capital and liquidity requirement for banks. If the capital base is inadequate and the supervisors impose a Pillar 2 requirement or Pillar 2 guidance (P2G), banks will have to build up capital. In addition, if necessary, banks may be required to improve their liquidity situation beyond the minimum legal requirements and/or remedy identified deficiencies. Together, these measures are designed to maintain financial stability by ensuring that banks will be sufficiently resilient even under adverse business conditions. Following up on the SREP process, supervisors will, in the process of off-site analysis, monitor banks’ compliance with the requirements and measures detailed in the SREP decisions. If required, they will also carry out on-site inspections.

SREP disclosures (SIs)

Under EU law, banks have to disclose their P2Rs on an annual basis.

In addition, the ECB publishes the consolidated P2Rs of all significant institutions (SIs) it supervises (see “Links”), setting out P2Rs and leverage ratio P2Rs for SIs.

Moreover, the results are presented in aggregated form to provide an overview of the capital requirements for all Single Supervisory Mechanism (SSM) banks (see “Links”). P2G, by contrast, is not published.

As for the P2R of less significant institutions (LSIs) in Austria, the aggregated SREP results as well as the methodological requirements can be found in the download section.

How is the principle of proportionality applied in the LSI SREP?

In principle, the SREP for LSIs uses the same methodology as for SIs. However, the intensity of supervision, i.e. the frequency, scope and granularity of analyses, varies depending on the size, complexity and riskiness of a bank’s operations. For example, applicable law normally requires that a full SREP assessment of small and non-complex institutions (SNCIs), including the provision of information on any quantitative and qualitative measures, be carried out every three years. Risk assessments are updated in the years between full assessments. The OeNB and FMA take a risk-based approach, i.e. the intensity of supervision can be increased for smaller banks if they have a worse risk profile.

A general high-level overview of the SREP methodology for LSIs can be found in the download section.

SREP disclosures (LSIs)

To enhance transparency and to give banks a general understanding of what their own results mean, aggregated SREP results for Austria’s LSIs are made available in the download section. The data is updated every year in the fall, providing information about the previous year’s results.